Long-term care insurance is one of the most complex types of insurance. Due to the intricacies of these policies it can be hard to determine if you are comparing apples-to-apples when searching for what may be best for you. To that end, we have included a list of questions to ask yourself, or the agent you are working with, in order to help better understand the costs and benefits.

What types of facilities are covered? Long-term care policies can cover the following types of care:

- Nursing home care

- Home health care

- Respite care

- Hospice care

- Personal care in your home

- Assisted living facilities

- Adult day-care centers

Many long-term care policies cover some combination of these. Be sure to understand what facilities are included when you’re considering a policy.

Due to the complexities of long-term care insurance we suggest working closely with a professional that has experience in this area.

What is the daily, weekly, monthly benefit amount? Policies normally pay benefits by the day, week, or month. You may want to evaluate what long-term-care facilities in your area are charging before committing to a policy.

What is the maximum benefit amount? Many policies limit the total benefit they’ll pay over the life of the contract. Some state this limit in years, others in total dollar amount. Be sure to address this question.

What is the elimination period? Benefits don’t necessarily start when you enter a nursing home. Most have an elimination period—a period during which the insured is responsible for the cost of care. In many policies, elimination periods can range from zero to one-hundred days after nursing home entry or disability.

Does the policy offer inflation protection? Adding inflation protection to a policy may increase its cost, but it could be important if long-term care services increase in price. In fact, for those looking to purchase a policy now for use in later years inflation protection can be a valuable planning tool.

How are benefits triggered? Insurance companies use specific criteria in order to determine when to trigger benefits. The most common trigger is the inability to complete a certain number of the activities of daily living (ADLs) without assistance. There are six activities of daily life that most insurance companies use. They are as follows:

- Bathing

- Continence

- Dressing

- Eating

- Toileting

- Transferring

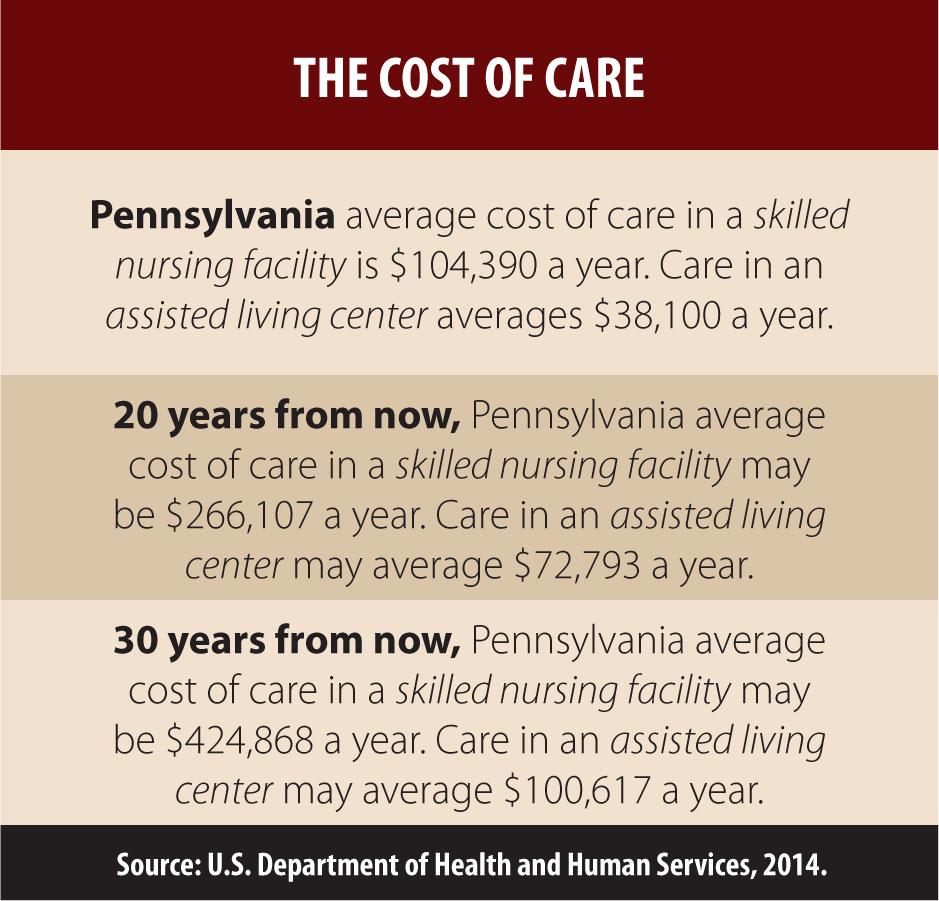

Click to enlarge

And, it is important to note that policies have benefits for Alzheimer’s disease, dementia, or other forms of cognitive impairment.

Is the policy tax qualified? Certain long-term care policies can offer federal income tax benefits. Generally, premiums paid for these policies can be included with other uncompensated medical expenses for deduction from income if they exceed 7½% of adjusted gross income. And benefits received generally will not be counted as income.

How strong is the insurance company? There are several companies that analyze the financial strength of insurance companies. The ratings can show you how industry watchers view various insurance companies.

There are many factors to consider when reviewing long-term care programs. The best policy for you may depend on a variety of factors. Due to the complexities of long-term care insurance it can be beneficial to work closely with an insurance expert that has the depth and level of experience required to help determine the best policy for your own unique situation. If you would care to learn more please contact our office at your convenience.

What other policy options are available? There are a number of other long-term care policy options you may want to consider. Waiver of premium allows premiums to be discontinued once benefits are triggered. Third-party notice requires the insurance company to notify a third party whenever premiums have been missed — so the insured can have a child or trusted advisor make certain that premiums are paid.