Click to enlarge

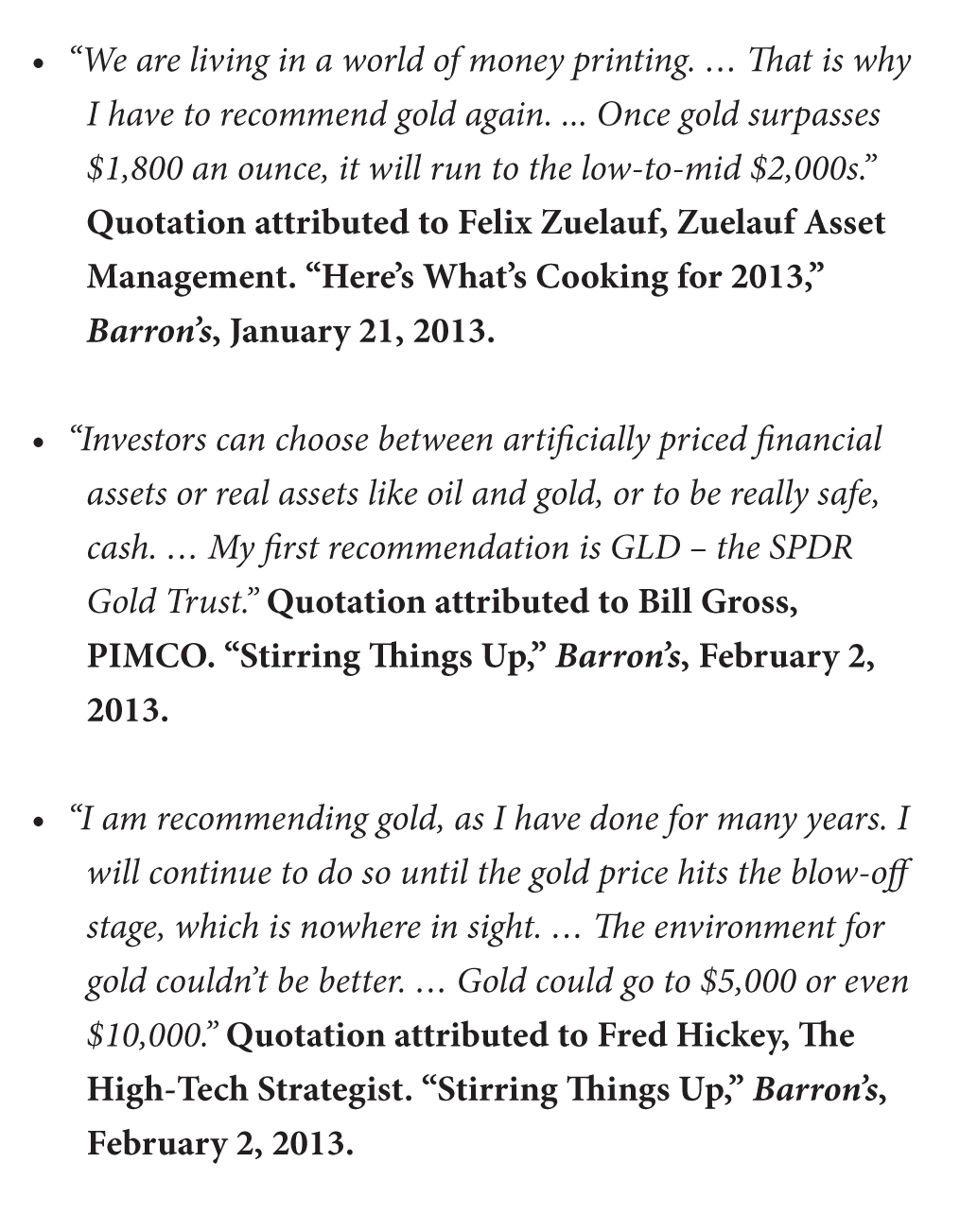

Each January, a group of prominent investment professionals gather in New York as members of the Barron’s Roundtable to trade quips, stock ideas, and the outlook for markets and economic trends worldwide. Barron’s—a weekly financial newspaper with a small but devoted following of professional and do-it-yourself investors—publishes a transcript of their remarks over three successive issues. The quotations to the right are excerpts from this year’s panel discussion, and to the best of our knowledge they represent the only occasion that three of the nine participants have highlighted gold-related investments among their choices for capital appreciation during the year ahead.

Although the year is far from over, it’s off to a rough start for gold enthusiasts. A sharp selloff in mid-April sent bullion prices to $1,395 on April 15, down 15.7% for the year to date and 26.4% below the peak of $1,895 reached in early September 2011. (Prices are based on the London afternoon fix.) For the 10-year period ending March 31, 2013, gold enthusiasts have a more positive story to tell: The annualized return for gold spot prices was 16.83%, compared to annualized total returns of 8.53% for the S&P 500 Index, 10.19% for the MSCI EAFE Index, 17.41% for the MSCI Emerging Markets Index, and 2.34% for the S&P Goldman Sachs Commodity Index.

Taking a somewhat longer view, for the 40-year period ending March 31, 2013, gold performed in line with many widely followed fixed income benchmarks, while lagging behind most equity indices. We find it ironic that the return on gold over the past four decades is essentially indistinguishable from five-year US Treasury notes, often scorned by gold advocates as “certificates of confiscation.”

Click to enlarge

Considering the volatility of gold prices, even a 40-year period is too short to provide conclusive evidence regarding gold’s expected return. And the issue is further clouded by shifts through time in the legality of gold ownership and its changing role in various monetary systems worldwide. In his book The Golden Constant, published in 1977, University of California, Berkeley Professor Roy Jastram examined the behavior of gold in England and America over a 400-year-plus period—and suggested that the long-run real return of gold was close to zero. Even with centuries of data to study, however, he couched his conclusions in cautious language.

When we last commented on gold in February 2012 (“Who Has the Midas Touch?”), the mysterious metal was changing hands at $1,770 per ounce. We directed readers’ attention to the Berkshire Hathaway 2011 annual report, which presented an engaging discussion by Chairman Warren Buffett on the long-term appeal of gold—or, in his view, the lack of it. Since that time, the role of gold in a portfolio has provoked vigorous debate in the investment community, with thoughtful, articulate, and successful investors lining up on both sides of the issue, including at least three billionaire hedge fund managers making the case for gold.

Some might argue that gold’s price behavior will never succumb to rational analysis. For those seeking to try, a recently updated paper by Claude Erb and Campbell Harvey offers a useful framework for discussion without necessarily resolving the debate. Along the way, it provides the reader with a few nuggets of historical interest, including a comparison of military pay between US Army captains of today and Roman centurions under Emperor Augustus. (Apparently, little has changed over 2,000 years.)

The authors cite a number of reasons advanced in support of gold ownership, including a hedge against inflation, a safe haven in times of stress, an alternative to assets with low real returns, and its “under-owned” status across investor portfolios. Although the inflation hedge argument is likely the most frequently cited attraction for gold investors, the authors find little evidence that gold has been an effective hedge against unexpected inflation. They go on to poke holes in the assertion that gold qualifies as a genuinely safe haven or presents an appealing alternative in a world characterized by low real yields.

The most interesting argument, they believe, is the claim that gold is under-owned in investor portfolios and that a small shift in investors’ allocation strategy could lead to a significant rise in the real price of gold. Putting aside for a moment the ambiguity of the “under-owned” statement (all the world’s gold is already owned by somebody), the authors suggest it is plausible that individuals or central banks could choose to have greater exposure to gold. If they are insensitive to prices, this choice could cause the real price of gold to rise, particularly if gold producers are unwilling or unable to increase production. (On that note, it’s also conceivable that a significant real price increase would encourage development of electrochemical extraction of the estimated 8 million tons of gold contained in the world’s oceans, dwarfing the existing gold supply.)

The “gold is under-owned” argument has been advanced by a number of thoughtful investors, and only time will tell if such a shift in allocation strategy takes place with the consequences they expect. While acknowledging the bullish implications for gold prices under this scenario, the authors point out that gold prices relative to the current inflation rate are roughly double their long-run average since the inception of gold futures trading in 1975. They suggest $800 per ounce is a suitable target when applying this metric. Which is more plausible—that prices will gravitate closer to their historical average or that a new world order is emerging that calls for a sharply different valuation approach? No one can be sure; hence, the title of their paper, “The Golden Dilemma.”

What should investors make of all this? In our view, long-run investment results for any individual reflect the combination of available capital market returns and the investor’s behavior and temperament. As Warren Buffett has observed, excitement and expenses are the enemy of every investor, and all of us could benefit by examining our inclination to invest with our hearts rather than our heads. The decision to own gold often is motivated by an emotional response to current events, leading to abrupt shifts in asset allocation strategy and a failure to achieve capital market rates of return there for the taking. If adopting a permanent 5% allocation to gold encourages investors to maintain a buy-and-hold strategy for the remaining 95% of their portfolio, perhaps that is the most sensible solution for some. Many other investors undoubtedly will be just as content to stock their portfolios with securities offering interest and dividends—and let gold fulfill their innate human desire for rare and beautiful objects of adornment.

About the Author:

Weston J. Wellington, a vice president with Dimensional, is another of the firm’s in-house research experts. He works closely with financial advisors in the US, Canada, Europe, Australia, and Latin America, showing them how a science-based “equilibrium” strategy is the most reliable way to achieve investment success and why their clients are unlikely to hear about this approach from the usual sources of financial advice.

References:

Jastram, Roy W. The Golden Constant, John Wiley & Sons, 1977.

Erb, Claude B., and Campbell R. Harvey. “The Golden Dilemma.” http://sssrn.com/abstract=2078535.

Barclays data, formerly Lehman Brothers, provided by Barclays Bank PLC.

Stocks, Bonds, Bills and Inflation Yearbook. Chicago: Ibbotson Associates.

MSCI data copyright MSCI 2013, all rights reserved.

S&P data provided by Standard & Poor’s Index Services Group.

Dimensional Index data compiled by Dimensional.

London gold fix prices: London Bullion Market Association. Accessed April 24, 2013. www.lbma.org.uk.

Gold spot prices: Bloomberg returns from composite prices.