Markets recently have had a rocky time as investors in aggregate reassess prospects for monetary policy stimulus in the US. Is this something to worry about?

The world’s most closely watched central bank unsettled financial markets by flagging that it may start to scale back its bond purchases later this year.

Under this program of so-called “quantitative easing,” the Fed buys $85 billion a month in bonds as a way to keep long-term borrowing costs down and help generate a self-sustaining economic recovery.

What spooked the markets was a comment by Fed Chairman Ben Bernanke on May 22 that the central bank may start to scale back those purchases in coming meetings.

The mere prospect of the monetary tap being turned down caused a reassessment of risk, leading to a retreat in developed and emerging economy equity markets, a broad-based rise in bond yields, and a decline in some commodity markets and related currencies, such as the Australian dollar.

Gold, in particular, was hit hard by the Fed’s signals, with the spot bullion price falling 23% during the second quarter on the view that rising bond yields and a strengthening US dollar would hurt the metal’s appeal as a perceived safe haven.

For the long-term investor, there are a few ways of looking at these developments.

First, we are seeing a classic example of how markets efficiently price in new information. Prior to Bernanke’s remarks, markets might have been positioned to expect a different message than he delivered. They adjusted accordingly.

Second, since the patient is showing signs of recovery, policymakers can publicly countenance a change in policy—“taking away the punch bowl.”

This is not to make any prediction about the course of the US or global economy. It just tells you that policymakers and investors are reassessing the situation.

Third, for all the people quitting positions in risky assets like stocks or corporate bonds, there are others who see long-term value in those assets at lower prices. The idea that there are more sellers than buyers is just silly.

Fourth, the rise in bond yields is a signal that the market in aggregate thinks interest rates will soon begin to rise. That is what the market has already priced in. What happens next, we don’t know.

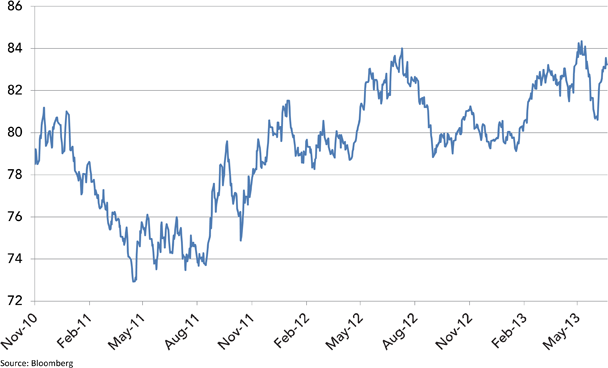

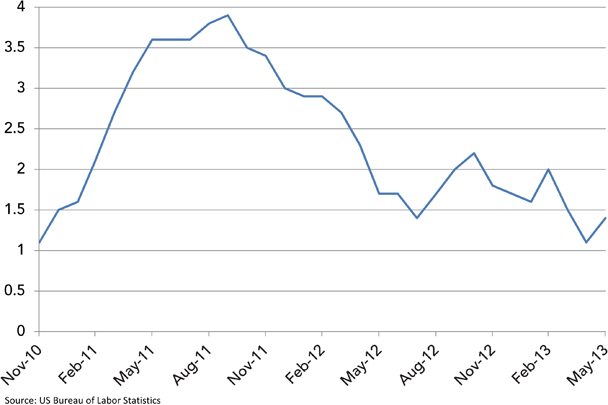

Keep in mind that when the Federal Reserve began its second round of quantitative easing in late 2010, there were dire warnings in an open letter to the central bank from a group of 23 economists about “currency debasement and inflation.”1

Yet, US inflation is now broadly where it was, and the US dollar is higher than when those warnings were issued (see charts below), suggesting basing an investment strategy around supposedly expert forecasts is not always a good idea.

US Dollar Index

Click to enlarge

US CPI Year-on-Year

Click to enlarge

So, it would pay to exercise skepticism with respect to predictions on the likely path of bond yields, interest rates, and currencies in the wake of the Fed’s latest signals. Just because something sounds logical doesn’t mean it’s going to happen.

Fifth, a rise in bond yields equates to a fall in bond prices. Just as in equities, a fall in prices equates to a higher expected return. So selling bonds after prices have fallen echoes the habit some stock market investors have of buying high and selling low.

Finally, keep in mind the volatility is usually most unnerving to those who pay the most attention to the daily noise. Those who take a longer-term, distanced perspective can see these events as just part of the process of markets doing their work.

After all, the individual investor is unlikely to have any particular insights on the course of global monetary policy, bond yields, or emerging markets that have not already been considered by the market in aggregate and built into prices.

What individuals can do, with the assistance of a professional advisor, is manage their emotions and remain focused on their long-term, agreed-upon goals.

Otherwise, you risk reacting to something that others have already countenanced, priced into expectations, and moved on from as further information emerged.

Inevitably, second-guessing markets means second-guessing yourself.

About the Author:

Jim Parker, a vice president in the Communications Group of Dimensional Fund Advisors presents strategies to communicate Dimensional’s philosophy and process in ways that engage clients, prospects, regulators, and the media. Jim holds an economic history degree from Deakin University and a journalism degree from Auckland Technical Institute.

References:

1. Floyd Norris, “Predictions on Fed Strategy that Did Not Come to Pass,” New York Times (June 28, 2013).