When the Tax Cuts and Jobs Act (TCJA) Act passed in 2017, we were told that all of the provisions—lower tax rates, much more generous estate tax exemption—would sunset at the end of 2025. That seemed a long way off back then. But now it’s 2024, less than two years before what could be a jarring shift in our tax regime. Soon, the top marginal tax rate is due to revert back to 39.6%. The standard deduction will drop to roughly half of today’s $14,600 (single) or $29,200 (joint). Most significantly, the estate tax exclusion—the amount that can be passed on to heirs without being taxed at the federal level—will drop from $13.61 million this year to somewhere around $6.5 million.

When the Tax Cuts and Jobs Act (TCJA) Act passed in 2017, we were told that all of the provisions—lower tax rates, much more generous estate tax exemption—would sunset at the end of 2025. That seemed a long way off back then. But now it’s 2024, less than two years before what could be a jarring shift in our tax regime. Soon, the top marginal tax rate is due to revert back to 39.6%. The standard deduction will drop to roughly half of today’s $14,600 (single) or $29,200 (joint). Most significantly, the estate tax exclusion—the amount that can be passed on to heirs without being taxed at the federal level—will drop from $13.61 million this year to somewhere around $6.5 million.

Of course, the sunset will not be all bad. After 2025, the $10,000 cap on state and local tax deductions will go away, the the limit on how much mortgage interest is deductible will go up from the first $750,000 in debt back to $1 million, and a bunch of miscellaneous itemized deductions, including investment/advisory fees, legal fees and unreimbursed employee expenses will be restored. People in lower income brackets will get back a personal exemption amount of (inflation-indexed) $4,700, phased out as taxable income goes up.

How should taxpayers prepare for these various changes, to take advantage of today’s rates or exemptions? The answer varies widely with individuals, but there are some strategies that are widely-applicable. Some tax experts with a terrible sense of humor say they are recommending that if their clients are in poor health, they should plan on dying before the sunset. Less macabre strategies include strategically taking capital gains out of taxable portfolios at today’s (and next year’s) lower tax rates, and holding off harvesting capital losses until 2026.

Families who might bump up against the lower estate tax exemption could gift assets from one spouse’s lifetime exemption while preserving the other spouse’s. Since these exemptions are portable, either spouse will be able to use the other one’s upon the death of one spouse, so nothing is lost by taking this route. There are various trust strategies that will move assets out of the taxable estate—the most-often-cited are the spousal lifetime access trust and the grantor-retained annuity trust, both of which use the gifted assets to provide lifetime retirement income to the donors.

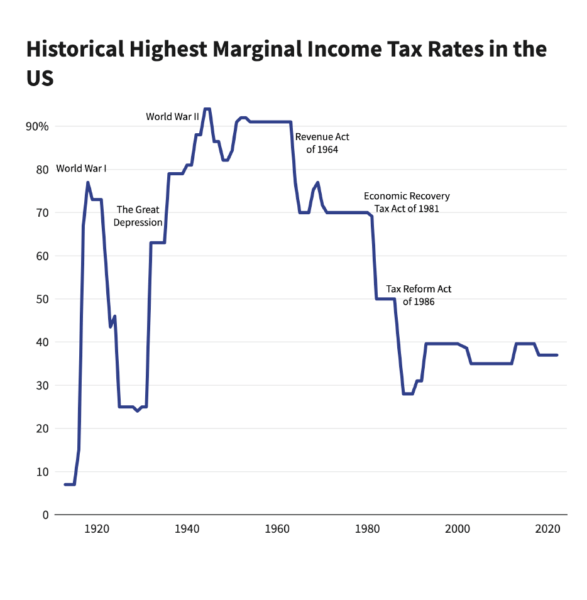

But as you consider these strategies with your advisor, it’s helpful to remember that Congress might intervene between now and January of 2026, and pass entirely new tax legislation. As you can see from the chart, it’s happened a few times before.