NOTE: This article uses an example of an event that occured in Australia, however similar parallels can be drawn to situations that have occured in the domestic U.S.

There are two ways of learning: You can be taught how to do something correctly, or you can be shown the consequences of doing it wrong. In the world of investment, it’s a lot cheaper to learn from others’ mistakes.

A recent edition of a television current affairs program1 detailed how elderly Australians, many of them with only modest nest eggs, had lost up to $15 billion in recent years through dubious investment schemes.

Most of these schemes involved the provision of high-risk finance to property ventures, some involving speculative residential projects. Yet, the program found, these investments were often promoted as safe, secure, and bank-like.

In some cases, the promoters of the schemes extracted high fees (as much as 5%) from the vehicles, and engineered related-party transactions that cost the clients millions—without giving them any say in the matter.

The program found that end investors often had their entire life savings in a single investment product, which meant there was no safeguard when things went wrong. On top of all this, the schemes were promoted by financial “advisors,” who earned commissions on their sales.

The wonder is that these dubious schemes continue to fleece thousands of people five years after the financial crisis exposed the folly of structured and highly conflicted mortgage finance vehicles and securities firms masquerading as banks.

In one heartbreaking moment in the program, a widow with an autistic son told how she lost $330,000 in compensation from the death of her husband after she was advised to put the money into a fund linked to a finance company that later failed.

The woman is now unable to afford the special education the boy needs and has called on her in-laws to provide emergency childcare while she works full time.

New regulations in Australia are about improving disclosure to investors and removing conflicts of interest around advice. But they have clearly come too late to help the thousands of people hurt by these collapses.

Most importantly, get truly independent advice. That means avoiding recommendations of someone who is receiving a financial or other incentive from the provider whose product he is promoting.

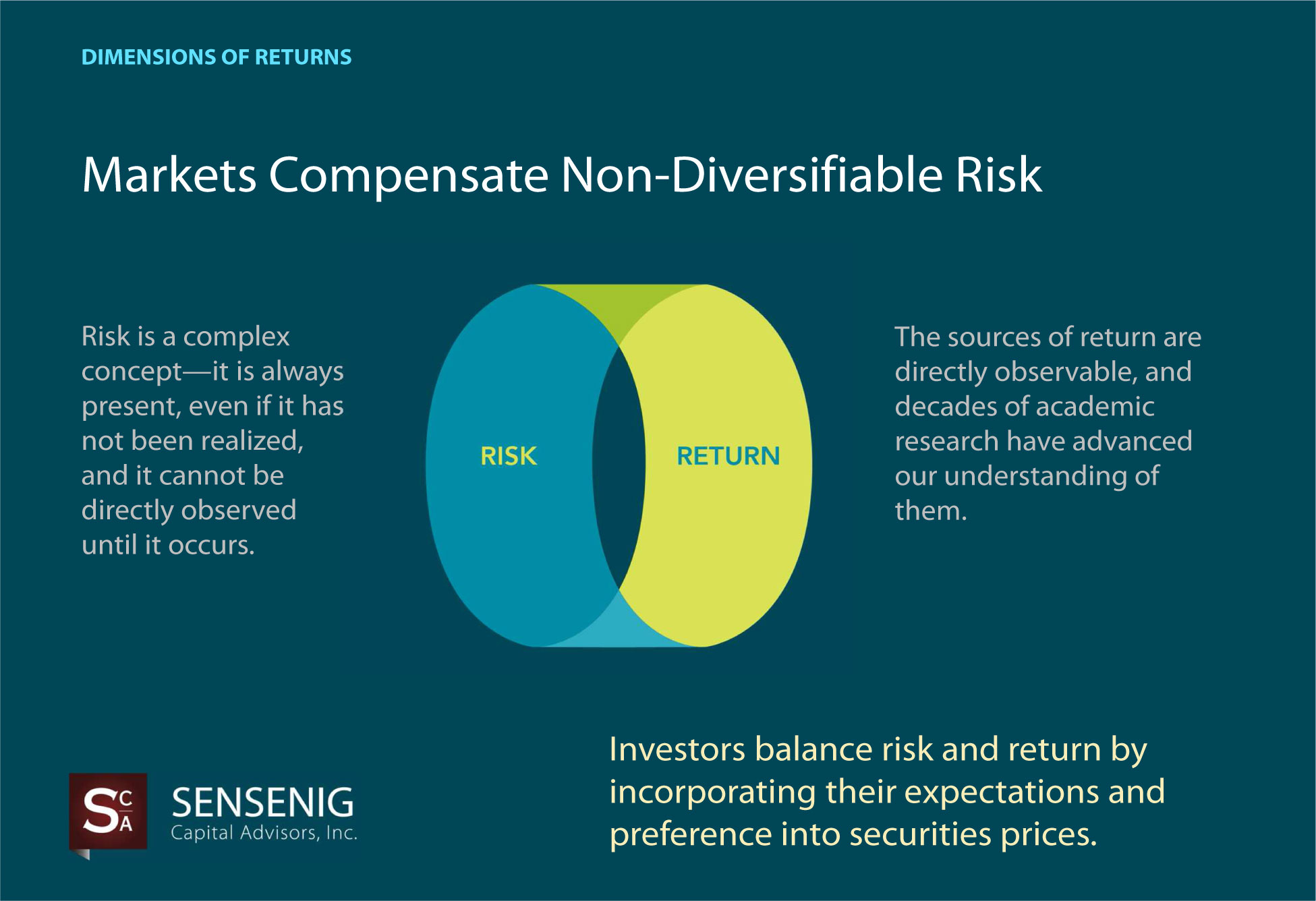

So, barring a further change in the law to protect against fraud, how can individual investors protect themselves? First, understand risk and return. If someone is offering a “low-risk” investment with a regular return well above the risk-free rate, alarm bells should go off. Return rarely comes without risk, but not all risks are worth taking. So always ensure you understand what you are investing in.

Second, diversify. It is the only free lunch you will get as an investor. Sinking your life savings into a single property scheme or mortgage fund is not diversification. That is taking a massive, speculative bet on a single asset.

It is far better for your long-term wealth to spread risk across a range of asset classes—domestic and developed markets equities, emerging markets, local and global bonds, listed property, and cash. And within each asset class, you should diversify as much as possible.

Click to enlarge

Third, fees matter. The difference made by a 1%, 2%, or 3% fee can run into hundreds of thousands of dollars over the years. Time after time, we see the rewards in these heavily marketed schemes going not to the end investors but to the promoters.

Finally, and most importantly, get truly independent advice. That means avoiding the recommendations of someone who is receiving a financial or other incentive from the provider whose product he is promoting.

A good advisor will work for you. That means understanding your risk appetites, your situation, and your investment and lifestyle goals. It means structuring a diversified portfolio that reflects your needs, not what a product provider has to sell.

The losses suffered by Australians in these schemes are tragic. Liquidators interviewed by the program had little hope that people would get much of their money back, if any. Questions were raised about the adequacy of regulation.

Ordinary investors can’t control those outcomes. But they can learn from these lessons and steer clear of anything that smells of conflicted advice, promises of high returns and low risk, lack of diversification, high fees, and slick marketing.

If we don’t learn these lessons from the experiences of others, we risk having them taught to us directly. In those cases, the tuition bills can be substantial.

1. “A Betrayal of Trust,” Four Corners, Australian Broadcasting Corp. Television, March 4, 2013.

This material may refer to resident trusts offered by DFA Australia Limited. These resident trusts are only available in Australia. Nothing in this material is an offer or solicitation to invest in these resident trusts or any other financial products or securities. All figures in this material are in Australian dollars unless otherwise stated.

About the Author: Jim Parker, a vice president in the Communications Group of Dimensional Fund Advisors presents strategies to communicate Dimensional’s philosophy and process in ways that engage clients, prospects, regulators, and the media. Jim holds an economic history degree from Deakin University and a journalism degree from Auckland Technical Institute.