While many market participants wait for the “inevitable” rise in short-term interest rates expected when the Federal Reserve tightens its monetary policy, some investors may have missed the increase in short-term rates already underway as a result of market forces.

Looking at the zero- to two-year segment of the yield curve—the segment that many believe will be most affected whenever the Fed “normalizes interest rates”—it may be surprising to see how much rates have increased since 2013.

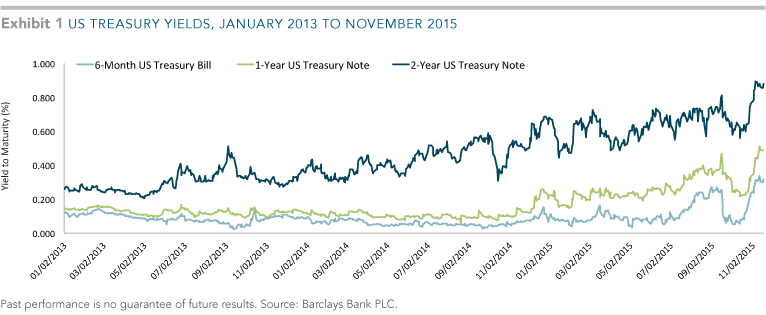

Click to enlarge

In fact, the yield on the 2-Year US Treasury note has nearly doubled since the beginning of 2015, rising from 0.45% in January to almost 0.90% today.* The yield on the 1-Year US Treasury note has more than tripled, from 0.15% to more than 0.50% over the same period. The 6-Month US Treasury bill’s yield rose from a low of 0.03% in May to over 0.30% today. Yet, despite the higher rates, we have not experienced the conjectured financial storm in the fixed income market.

The question of when the Fed will raise its overnight target rate is still open. Similarly, we can ask ourselves a more complex question: Will the market lead the Fed or is the Fed leading the market through setting expectations?

*As of November 18, 2015. Source: Barclays Bank PLC.