Global markets are providing investors a rough ride at the moment, as the focus turns to China’s economic outlook. But while falling markets can be worrisome, maintaining a longer term perspective makes the volatility easier to handle.

A typical response to unsettling markets is an emotional one. We quit risky assets when prices are down and wait for more “certainty.”

These timing strategies can take a few forms. One is to use forecasting to get out when the market is judged as “overbought” and then to buy back in when the signals tell you it is “oversold.”

A second strategy might be to undertake a comprehensive macro-economic analysis of the Chinese economy, its monetary policy, global trade and investment linkages, and how the various scenarios around these issues might play out in global markets.

In the first instance, there is very little evidence that these forecast-based timing decisions work with any consistency. And even if people manage to luck their way out of the market at the right time, they still have to decide when to get back in.

In the second instance, you can be the world’s best economist and make an accurate assessment of the growth trajectory of China, together with the policy response. But that still doesn’t mean the markets will react as you assume.

A third way is to reflect on how markets price risk. Over the long term, we know there is a return on capital. But those returns are rarely delivered in an even pattern. There are periods when markets fall precipitously and others when they rise inexorably.

The only way of getting that “average” return is to go with the flow. Think about it this way. A sign at the river’s edge reads: “Average depth: three feet.” Reading the sign, the hiker thinks: “OK, I can wade across.” But he soon discovers the “average” masks a range of everything from 6 inches to 15 feet.

Likewise, financial products are frequently advertised as offering “average” returns of, say, 8%, without the promoters acknowledging in a prominent way that individual year returns can be many multiples of that average in either direction.

Now, there may be nothing wrong with that sort of volatility if the individual can stomach it. But others can feel uncomfortable. And that’s OK too. The important point is being prepared about possible outcomes from your investment choices.

Markets rarely move in one direction for long. If they did, there would be little risk in investing. And in the absence of risk, there would be no return. One element of risk, although not the whole story, is the volatility of an investment.

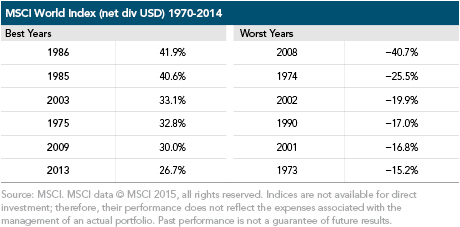

Look at a world stock market benchmark such as the MSCI World Index, in US dollars. In the 45 years from 1970 to 2014, the index has registered annual gains of as high as 41.9% (in 1986) and losses of as much as 40.7% (2008).

But over that full period, the index delivered an annualized rate of return of 8.9%. To earn that return, you had to remain fully invested, taking the unsettling down periods with the heartening up markets, but also rebalancing each year to return your desired asset allocation back to where you want it to be.

Timing your exit and entry successfully is a tough task. Look at 2008, the year of the global financial crisis and the worst single year in our sample. Yet, the MSCI World index in the following year registered one of its best ever gains.

Now, none of this is to imply that the market is due for a rebound anytime soon. It might. It might not. The fact is no one can be sure. But we do know that whenever there is a great deal of uncertainty, there will be a great deal of volatility.

Second-guessing markets means second-guessing news. What has happened is already priced in. What happens next is what we don’t know, so we diversify and spread our risk to match our own appetite and expectations.

Spreading risk can mean diversifying within equities across different stocks, sectors, industries, and countries. It also means diversifying across asset classes. For instance, while stocks have been performing poorly, often bonds have been doing well.

Markets are constantly adjusting to news. A fall in prices means investors are collectively demanding an additional return for the risk of owning equities. But for individual investors, the price decline, if temporary, may only matter if they need the money today.

If your horizon is 5, 10, 15, or 20 years, the uncertainty will soon fade and the markets will worry about something else. Ultimately, what drives your return is how you allocate your capital across different assets, how much you invest over time, and the power of compounding.

But in the short term, the greatest contribution you can make to your long-term wealth is exercising patience. And that’s where your advisor comes in.