Interest rates around the world are at historic lows. They can only go in one direction from here, right? And aren’t rising interest rates bad for bond investors? The truth might surprise you.

Central banks in developed economies have injected extraordinary stimulus into the system since the recession arising from the global financial crisis five years ago.

The stimulus has come from these steep reductions in official interest rates and from more unconventional measures aimed at holding down long-term interest rates.

In 2013, markets became unsettled when the US Federal Reserve signaled it was contemplating a timetable for reducing its stimulus—the so-called “taper.” The central bank later changed its mind, and markets cheered the news.

In the meantime, many investors are asking what will happen to their portfolios when central banks do decide to start restoring rates to more normal levels.

The market values of bonds rise or fall depending on investors’ views about the outlook for inflation and interest rates, their perceptions about the creditworthiness of individual issuers, and their general appetite for risk.

The yield on a bond is the inverse of its price. So if the price falls, it means investors are demanding an additional return, or yield, on that bond to compensate for the risk of holding it to maturity. This sensitivity to interest rate change is called term risk.

So if interest rates can only go up from current levels, why hold bonds? There are a few points to make in response.

First, it is very hard to forecast interest rates with any consistency. Standard & Poor’s regular scorecard shows most traditional forecast-based managers fail to outpace bond benchmarks over periods of five years or more.1

Second, there is nothing to say that rates will return to normal very quickly. In the case of Japan, benchmark lending rates have been at or close to zero for the best part of 15 years. We have already seen many large bond fund managers make badly timed calls on when the cycle will turn.

Third, bonds perform differently from stocks. So regardless of what is happening with the rate cycle, there is a diversification benefit in holding bonds in your portfolio. Diversification is a way of managing risk and helping to target a smoother ride.

Fourth, if you look at history, there is no guarantee in any case that longer-term bonds will underperform shorter-term bonds when interest rates are rising.

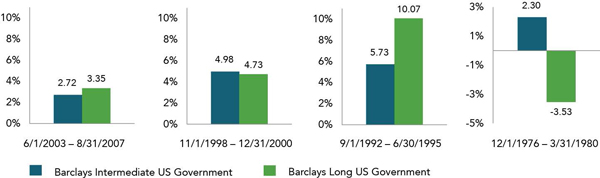

We carried out a case study of four periods of rising rates from the past 30 years. To meet the test, the rate increases had to be spread out over 12 months or more and cumulative increase had to be at least 1.5 percentage points.

The four periods were December 1976–March 1980 (when rates skyrocketed by 15.25 percentage points), September 1992–June 1995 (3 points), November 1998–December 2000 (1.75 points) and June 2003–August 2007 (4.25 points).

The chart below looks at the performance of US government bonds during those four periods. We use standard indices: the Barclays Intermediate (1–10-year maturity, in blue) and the Barclays Long (10–30-year maturity, in green).

Government Bonds: Annualized Total Returns

Click to enlarge

Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. Performance data shown represents past performance and is no guarantee of future results. Performance for periods greater than one year is annualized. For illustrative purposes only. Source: Barclays Capital data provided by Barclays Bank PLC.

What’s notable in the chart is that in two of these four periods of rising interest rates long-term bonds didbetter than shorter-to-intermediate-term bonds. In the other two periods (1998–2000 and 1976–1980), longer-term bonds underperformed.

This may seem counterintuitive, but it can be explained by the fact that long-term bond holders, whose biggest concern is inflation, can be comforted by a central bank moving aggressively and pre-emptively against this threat by raising official rates.

Also note that seven of these eight bars show positive returns, which contradicts the view that bonds always deliver negative returns in periods of rising interest rates. The exception in this study is the late 1970s, when the longest-term bonds (10–30 years) suffered during a period of very sharp increases in rates.

So, the first lesson is that an increase in official lending rates set by central banks is not always replicated across bonds of all maturities. Indeed, in some cases, as we have seen, longer-term bonds have outperformed in rising rate environments.

The second lesson is that bonds can play an important role in your portfolio whatever the stage of the interest rate cycle. How much term (or credit) risk you take with bonds will depend on your own risk appetite and investment goals.

Trying to forecast interest rates is not a sustainable way of investing in bonds. But there is plenty of information in today’s prices on which to base a strategy. In the meantime, you can help temper risk by diversifying across different types of bonds, different maturities, and different countries.

Ultimately, the reasons for investing in bonds should be driven by your own needs, not by everybody else’s expectations.

References:

1. Source: Standard & Poor’s Indices Versus Active Funds Scorecard, year-end 2012

About the Author:

Jim Parker, a vice president in the Communications Group of Dimensional Fund Advisors presents strategies to communicate Dimensional’s philosophy and process in ways that engage clients, prospects, regulators, and the media. Jim holds an economic history degree from Deakin University and a journalism degree from Auckland Technical Institute.