The sudden downward lurch in the stock market shone a brief spotlight on something called the Yen carry trade, which was cited as one of the causes of the selloff. But what, exactly, are we talking about?

The sudden downward lurch in the stock market shone a brief spotlight on something called the Yen carry trade, which was cited as one of the causes of the selloff. But what, exactly, are we talking about?

On the surface, the yen carry trade looks like a way to print money. The Bank of Japan has kept interest rates at or near zero for decades—which means that Japanese banks basically offer free money to borrowers. A hedge fund can borrow from a Japanese bank (whose currency is the yen), and then buy Treasury bonds that are paying, let’s say, 5%. 5% yields minus zero percent borrowing costs, with almost no risk, is a pretty nice risk-adjusted return. And the return is actually greater because, notice, very little of the hedge fund’s money is actually invested. This is borrowed money.

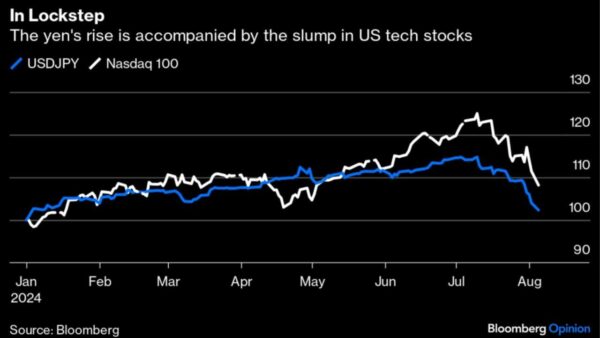

But of course hedge funds aren’t interested in 5% annualized returns on their borrowed money, and so they invest more adventurously—in, say, tech stocks. And apparently they have been doing a lot of this; the graph shows that the yen’s borrowing cost has closely tracked the price movements of U.S. tech stocks this year. The downtrend of both (right side of the graph) represents a move by the Bank of Japan to raise interest rates, creating actual, measurable costs to the leveraged yen borrowing activities.

How big is this carry trade thing? Put another way, is it possible that another rate rise by the Bank of Japan will wreak additional havoc on the U.S. markets? A recent report found that Japanese banks have lent foreign investors and others roughly $1 trillion up to the first quarter of the year. That’s about one-fiftieth of the aggregate value of U.S. stocks, which doesn’t sound too concerning until you realize that it only takes a handful of sales to start a trend and spook the investor herd—hence a small unwinding being blamed for a 3% drop in a broad-based U.S. index.

This is not a prediction, of course, and any unwinding will inevitably be picked up by other investors. None of this will affect the underlying value of U.S. companies. It’s a reminder that forces that have nothing to do with the underlying value of your investments can cause them to lurch periodically in unpredictable ways.