The media occasionally locks in on a particular “hot” sector. In the late 1990s, it was technology. In the mid-2000s, it was mining. Writing headlines about fashionable sectors is one thing. Building investment strategies around them is another.

A reason journalists focus on particular industries or sectors is that these stories fit into a chosen narrative. In the case of the tech stocks boom, it was the information revolution. In the case of mining stocks, it was the rise of China.

There’s nothing wrong with this kind of analysis, by the way. The lift in productivity brought by digital technology and communication was a real story, as was the impact of China as it integrated into the world economy over the past decade.

Where it goes wrong for investors is when they extrapolate from well-documented economic trends in order to make changes to their portfolios based on what has already happened or speculation about what might happen in the future.

In the Australian share market, for instance, mining stocks boomed in the first part of the last decade amid voracious demand for coking coal and iron ore from Chinese steelmakers (who produce 45% of steel globally).

By 2008, the boom was making billionaires of mining entrepreneurs like Andrew ‘Twiggy’ Forrest and Gina Rinehart. While Texas had its oil tycoons, wrote a Reuters reporter, the road to mega-riches in Australia ran through red dirt iron ore towns.1

At the time, Forrest’s listed company, Fortescue Metals Group, was so hot that it launched a 10-for-one stock split to take advantage of strong interest among smaller retail investors. The shares had quadrupled in value in less than a year.

The performance of stocks such as Fortescue mirrored what was going on in the commodity markets they serviced. Coal and iron ore prices had roughly tripled in Australian dollar terms in the six years up to mid-2008, with these bulk commodities by that stage accounting for nearly 30% of the Australian economy’s total exports.2

The heat around commodities continued to intensify over the next couple of years. By March 2010, London’sTelegraph newspaper predicted a further doubling in ore prices within months, stating the outlook for the sector was “very sunny indeed.”3

Desperately seeking cheaper supplies, Chinese companies went on an acquisition spree. In July 2010, theWall Street Journal said acquisitions by companies based in China or Hong Kong had grown hundredfold in five years.4

By 2012, though, iron ore prices were starting to fall from historic highs as China’s economic expansion slowed. Chinese steelmakers, in annual contract negotiations, sought to pay prices that better reflected the fall in the spot market.

Even so, Australian mining companies remained bullish. In an interview with the Australian, BHP Billiton’s head of iron ore forecasted that the spot price would settle around $120 (USD) a metric ton, down from the record of about $180 (USD).5

That wasn’t to be the case. Indeed, as the chart shows, iron ore prices collapsed, falling by two-thirds to below $60 (USD) by 2015. Chinese demand peaked just as new growth in global supply was coming online, a legacy of the long lead times in mining investment.

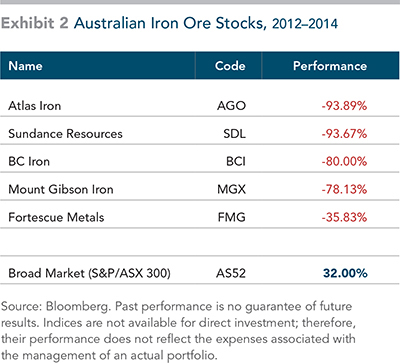

The market prices of mining stocks followed suit. On the Australian market during 2012–2014, many of the worst performing stocks have been either iron ore miners or companies serving that market, as shown in Exhibit 1.

This all goes to show the dangers of building investment strategies around sector stories. The iron ore companies were leveraged to China’s steel-making boom. They invested heavily in new capacity to take advantage of high prices.

But China’s boom started to wind down just as new mining capacity was coming on line. The double whammy from weakening demand and surging supply pummeled iron ore prices and drove down the market values of the mining stocks.

This is all another argument for the virtues of diversification. The more sector-specific risk and company-specific risk in a portfolio, the more it is exposed to these idiosyncratic factors beyond the control of the individual investor.

Diversification involves spreading risk and diluting the influence of sector-specific themes. So, just as miners and energy stocks have struggled in the past three years, other sectors such as healthcare, telecoms, and financials have done well.

But diversification does not just apply to sectors. We can also manage it by diversifying across the dimensions of returns, identified by academic research as the basic organizing principles of the market.

These “dimensions” point to systematic differences in expected returns. To meet this definition, they must be shown to be sensible, persistent across different periods, pervasive across markets, and capable of being cost-effectively captured.

The four dimensions are the degree to which the portfolio is exposed to stocks vs. bonds, small vs. large companies, low relative price stocks vs. high relative price, and high vs. low profitability firms.

In the small cap end of the Australian market, where many of the underperforming mining companies have crowded, some of the risk may be managed by excluding companies with the lowest profitability and those with the highest relative prices.

Of course, this does not mean a portfolio will be completely immunized against security-specific risk. But it is a way of diluting those influences and finding a balance between seeking to improve expected returns and striving for appropriate diversification.

At the end of the day, nothing in investment is ever cast in iron. But diversification, discipline, and maintaining a level of flexibility can help ensure that a single sector doesn’t bend your portfolio out of shape.

References:

1. “Australian Billionaires’ Row Paved in Iron Ore,” Reuters, January 9, 2008.

2. “Australia and the Global Market for Bulk Commodities,” Reserve Bank of Australia, January 2009.

3. “Iron Ore Price Could Almost Double by April,” The Telegraph, March 7, 2010.

4. “Chinese Firms Snap Up Mining Assets,” Wall Street Journal, July 20, 2010.

5. “Miners Still Bullish on China Demand,” The Australian, March 20, 2012.